For many people, the sale price of a particular home is the number that is most important to them. While knowing the cost of a house is crucial during the entire process of home buying in order to stay within budget, it is only one aspect that needs to be considered.

Knowing the interest rate — and shopping around for the best one — is another valuable factor. In fact, a home that offers a selling price that seems affordable could quickly balloon in cost so much that it is no longer within budget.

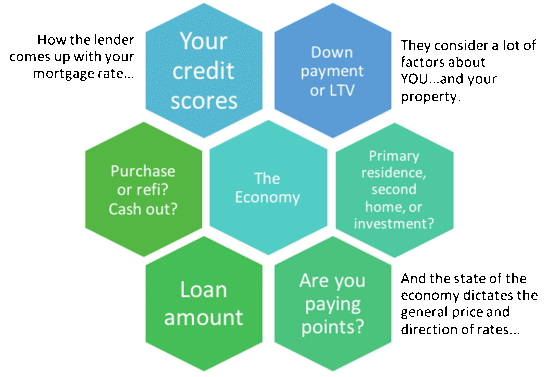

How the Interest Rate Affects the Purchase of a Home

In addition to the monthly mortgage payment, the typical home buyer also pays interest against the principal that was borrowed. The lower the interest rate, the less the home will cost of the life of the loan.

It is infinitely better to take the time to find the lowest interest rate possible when purchasing a new home. On the other hand, it is often worth the fees to refinance the loan at a later date if interest rates fall or better rates are found.

A lower interest rate can also increase a home buyer’s purchasing power because less of their monthly income will be earmarked for the mortgage payment. This means that it’s possible for the buyer to be able to afford a home that’s more expensive than they originally thought.

While a low interest rate is always a welcome addition to any home buying experience, it is especially helpful when the market prices are high. When coupled with a low mortgage rate, even home prices that might seem to be too high can become more affordable.

Determining the best interest rate by opting for a rate quote before shopping for a home puts buyers in a more attractive position. It also makes it more likely that they’ll be able to realize their dream of becoming homeowners.

Protected with 256 bit SSL

Protected with 256 bit SSL